- Fama, Eugene F. and French, Kenneth R., Long-Horizon Returns (November 20, 2017). Chicago Booth Research Paper No. 17-17, Fama-Miller Working Paper, Available at SSRN: https://ssrn.com/abstract=2973516 or http://dx.doi.org/10.2139/ssrn.2973516

- Siegel, Jeremy J. "The Long-term Returns on the Original S&P 500 Firms." The Journal of Finance, vol. 53, no. 6, 1998, pp. 2105-2128. doi: 10.1111/0022-1082.00075.

-

We use 60% as a threshold for being heavily concentrated in stocks due to the historically higher volatility of stocks compared to other asset classes. A study from AQR found that even in a fairly conservative portfolio consisting of 55 percent stocks and 45 percent other assets, that 55 percent in stocks carries 87 percent of the portfolio’s risk. To give an overly simplistic example, if you have a portfolio with 60% in stocks and 40% in cash, the cash isn’t likely to go down by 20% in a year whereas this type of behavior is well within the norm for stocks. Most other common asset classes (e.g. bonds, real estate) have historically had much lower volatility than stocks. That means most of the “risk” - that your portfolio's value could fall - is in the stocks holdings.

Generally the terms “risk” and “volatility” are used interchangeably in finance because the Capital Asset Pricing Model defines risk as the volatility of returns. The concept of “risk and return” is that riskier assets should have higher expected returns to compensate investors for the higher volatility and increased risk. Though I could write another paper on the many issues with equating volatility and risk, I will use the terms here identically as one can only fight so many battles at a time.

- Reid, Jim, Nick Burns, et al.. “The Age of Disorder.” Deutsche Bank Research, 8 Sept. 2020, www.epge.fr/wp-content/uploads/2020/09/The-age-of-disorder.pdf.

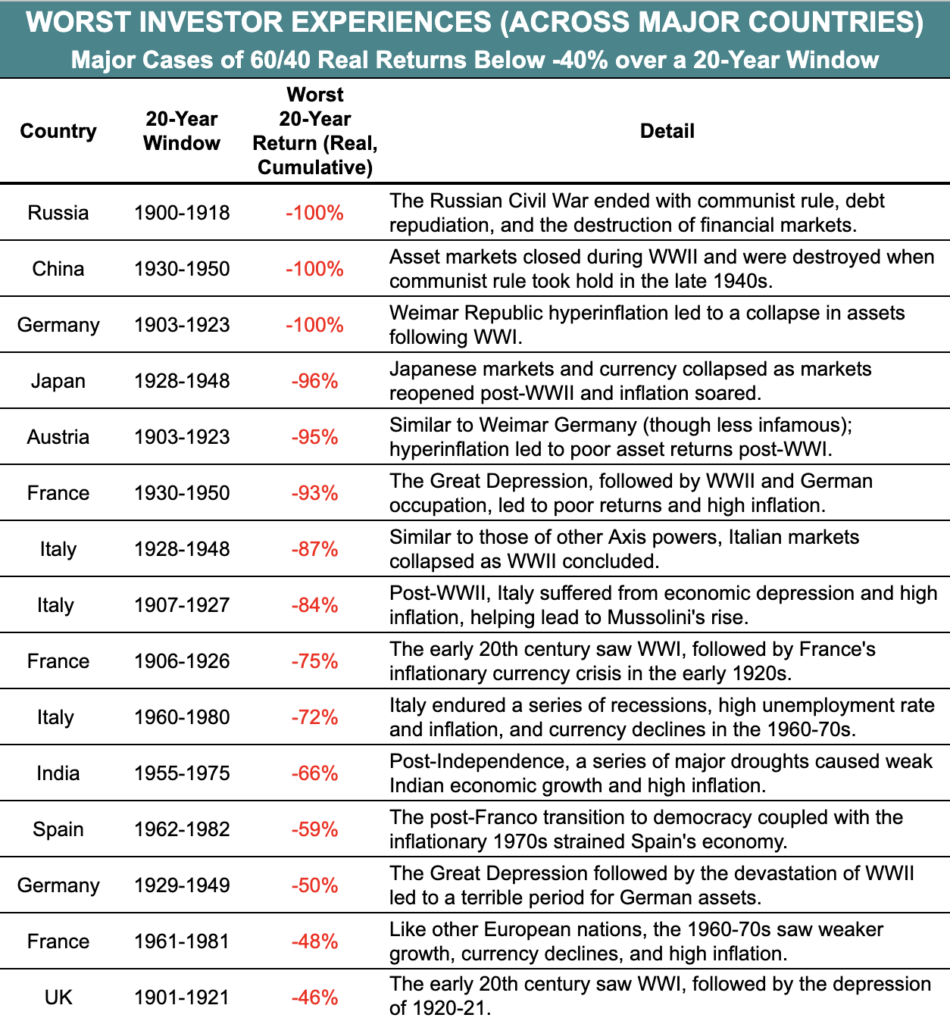

- Anarkulova, Aizhan and Cederburg, Scott and O'Doherty, Michael S., Stocks for the Long Run? Evidence from a Broad Sample of Developed Markets (January 18, 2021). Proceedings of Paris December 2020 Finance Meeting EUROFIDAI - ESSEC, Journal of Financial Economics (JFE), Forthcoming, http://dx.doi.org/10.2139/ssrn.3594660

- Dimson, Elroy, et al. "Stocks for the Long Run? Evidence from a Broad Sample of Developed Markets." Journal of Portfolio Management, vol. 28, no. 2, 2002, pp. 110-120. doi: 10.3905/jpm.2002.319361.

- Ibid. The authors noted that there is a survivorship bias in that continuous stock return data from successful markets are more readily available. The sample used in the study achieves substantially greater coverage of developed country periods compared to previous studies to minimize this bias. Survivor bias can lead to an upward bias in performance relative to ex-ante expectations (Brown et al., 1995). To combat survivor bias, researchers used a classification of developed countries and treatment of return data that doesn't condition on eventual market outcomes. Before 1948, countries entered the developed sample when their agricultural labor shares declined below 50%, drawing on evidence about labor patterns from the economics literature (e.g., Kuznets, 1973). After 1948, researchers used membership in the Organisation for Economic Co-operation and Development (OECD) and its European predecessor, the Organisation for European Economic Co-operation (OEEC). The treatment of return data in instances of market disruptions and failures (e.g., the temporary closure of stock exchanges or the permanent disappearance of the stock market in Czechoslovakia) reflects investor experiences to minimize survivor bias.

-

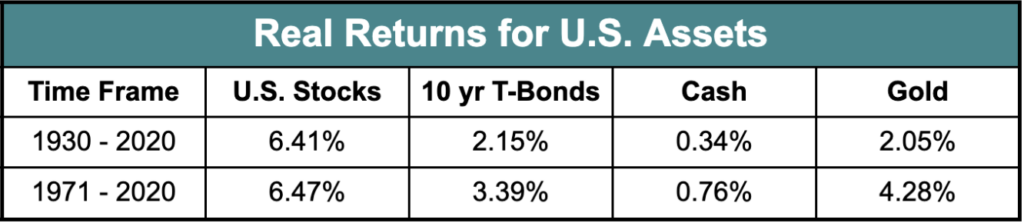

Return numbers can be cited in nominal and real terms. The nominal rate of return is the percentage return you see on your investments before accounting for inflation. For example, if you invested $100 and earned $105 after a year, your nominal return would be 5% ($5 profit/$100 invested).

However, inflation tends to gradually increase prices over time. So even though you earned 5% nominally, because of inflation, you may have slightly less buying power than when you first invested.

The real rate of return adjusts for inflation by subtracting the inflation rate from the nominal return. So if inflation was 3% in the year you earned 5% nominally, your real return would be about 2% (5% nominal - 3% inflation = 2% real). (Aside: this is not quite correct. Since inflation & returns compound, the full formula is ((1+return)/(1+inflation))-1. The end result is pretty close to the same and you get the idea)

This real rate of return reflects how much your buying power has actually increased after accounting for inflation. While the nominal return is the straight percentage gain, the real return better represents the growth in what your money can actually buy.

So in summary, the nominal return is just the simple percentage gain, while the real return adjusts for inflation to show how your purchasing power changed. I try to use real returns where available in this paper though it is not always feasible.

- Anarkulova et al.

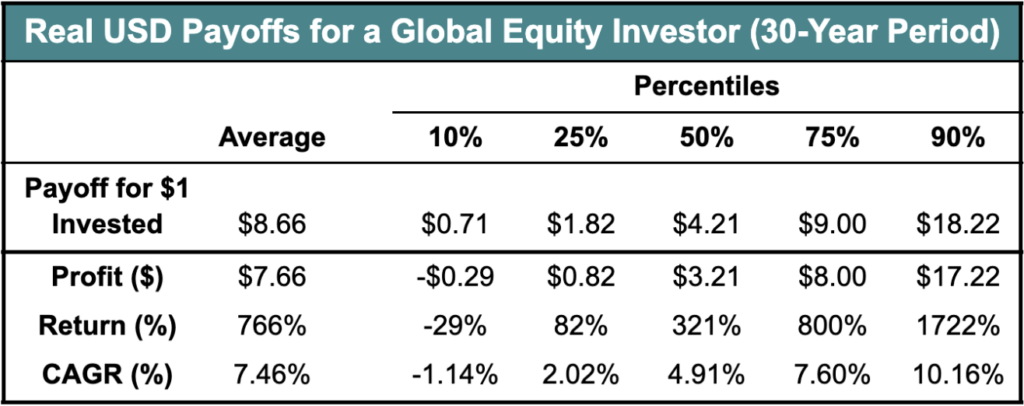

- The table summarizes the distribution of real payoffs from a $1.00 buy-and-hold investment across 1,000,000 bootstrap simulations at various return horizons. The underlying sample is the pooled sample of all developed countries. The real payoffs shown here are from the perspective of a global USD investor. Please see Anarkulova et al. for important information on sources and calculations.

- As a quick math refresher, the average return is the mean and is quite a bit higher than the 50th percentile because there are a few very good outcomes that make it higher. Percentiles are a way of ranking data points in a set from lowest to highest. They tell you what percentage of the data is below a certain value. For example, the 25th percentile means an investment return below which 25% of all returns fall. So in this example, the 25th percentile means 25% of simulations did worse and 75% did better. The 99th percentile means 99% of all simulations did worse and only 1% better. The 50th percentile is the median outcome.

- If not, consider a river which is 1 ft deep over 95% of its area, but contains a central channel that is 20 ft deep with a fast moving current. On average, it is ~2ft deep, but you can still drown in the main channel.

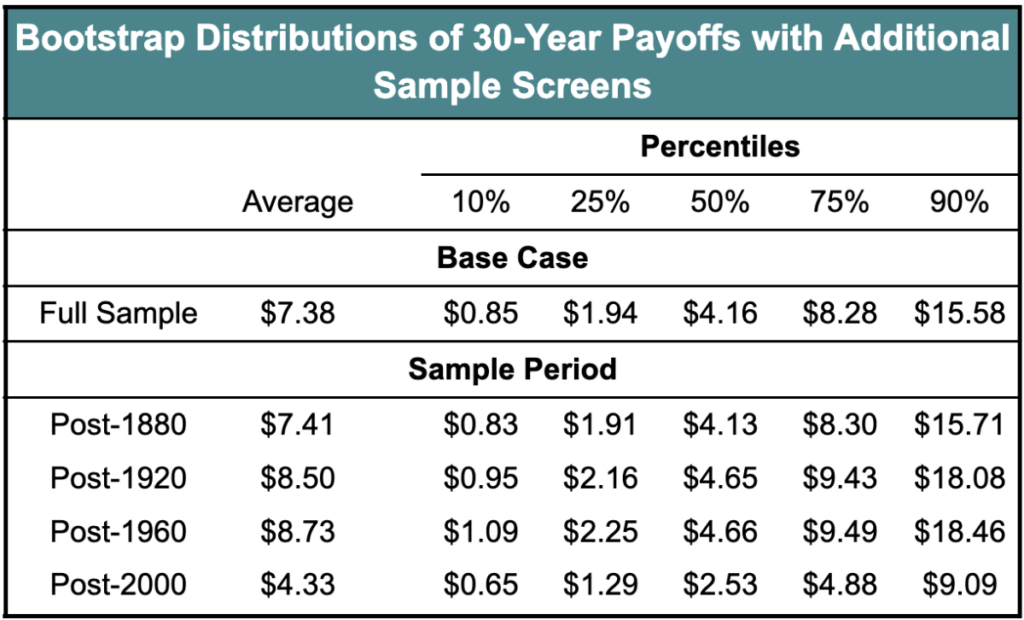

- Anarkulova et al.