The question of what you should invest in is, of course, unique to your situation. Nothing we say here can or should be considered a substitute for speaking with a financial advisor and the use of your own judgment. Having said that, we will offer a few ways of how we personally think about it.

In our opinion, the Cockroach Strategy is the best liquid total portfolio solution for those looking to maximize long-term compound growth while reducing drawdowns.

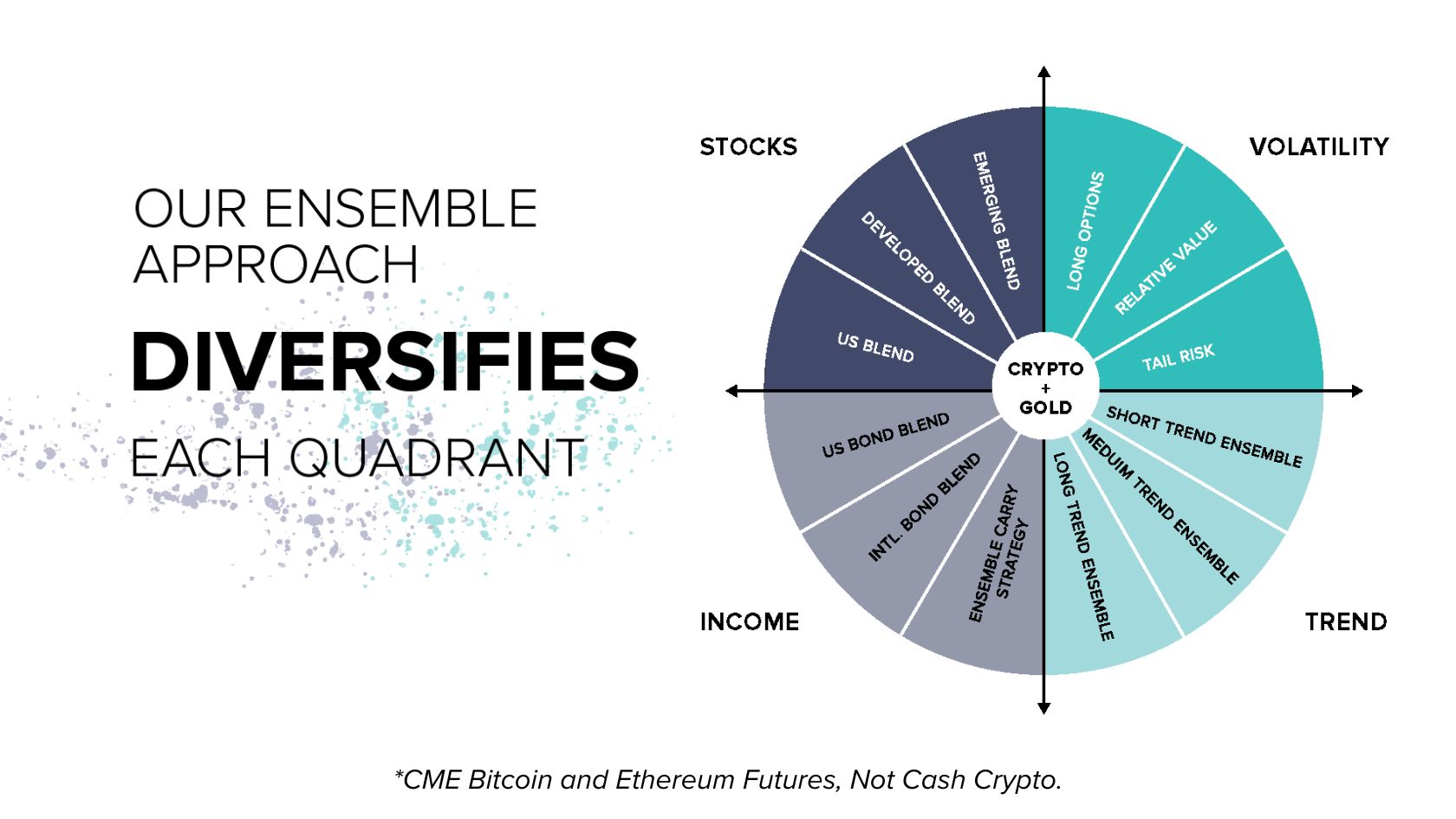

The way we look at it is that the best portfolio should perform across all major macroeconomics environments: Growth, Deflation, Decline and Inflation.

We believe that this requires roughly equal parts offense and defense.

Offensive assets would be assets such as public equities, angel, private equity, and real estate.

Defensive assets would be assets such as the Volatility Strategy, gold, commodity trend strategies, and cash.

The Cockroach Strategy seeks to provide exposure to a diversified ensemble of offense and defensive assets in a liquid portfolio.

In our view, Mutiny Funds’ other offerings including the Defense Strategy, Volatility Strategy, Volatility+Stocks Strategy, and Commodity Trend Strategy are best used as tools for investors which want to customize other parts of their portfolios within the Cockroach framework.

For instance, an investor that focuses on stock selection and wants discretion over the stock portion of their portfolio could do so as they see fit and use the Volatility Strategy, Trend Strategy, or Defense Strategy to complement it and provide their defensive exposure.

Similarly, an investor focused on income from Real Estate may want to manage the Income component themselves through their real estate holding and could use the Volatility+Stocks Strategy as well as the Trend Strategy to round out the portfolio.

Of course, you may have differing views on what the appropriate portfolio construction is for your situation and should allocate using your own judgment.

In the Cockroach Strategy, we will automatically rebalance the assets each month. For investors wishing to implement themselves, we believe they must rebalance regularly to achieve the best results. This means adding to the strategies when they are losing money as well as redeeming when they are performing well.

If you are investing through a retirement account, the rebalancing can be difficult to do since sometimes new funds cannot be transferred in when you would like to and so the Volatility+Stocks Strategy or Cockroach Total Portfolio Strategy may be more appropriate as the rebalancing is done “in house.”

We don’t believe in trying to time our exposures. For instance, Calpers missed a billion dollar payday in March 2020 when they redeemed their tail risk exposure just months before. Our philosophy is that investors should focus on building a balanced portfolio rather than trying to time macroeconomic trends.

Rather than engaging in market timing, we believe it is important to remember that the Volatility Strategy, Trend Strategy or any other component of the Cockroach Portfolio should be seen as part of a broader portfolio and viewed holistically.

There will be periods where Mutiny Funds’ Volatility Strategy or any long volatility strategy underperforms short volatility strategies and/or outright loses money. Similarly, there will be periods where Mutiny Funds’ Commodity Trend Strategy underperforms or suffers losses. However, what matters is how it is performing its role in the portfolio. If a long volatility strategy is struggling while the rest of the portfolio is doing well, that’s nothing to be unhappy about – indeed that is part of its role.

We strongly believe that the combination of long and short volatility strategies will produce the best risk-adjusted returns over the long run of a lifetime, a form of True Diversification.

In the normal course of business, we are able to offer monthly liquidity. That means that if we get 8 business days’ notice before the end of the month, we are able to send the majority of your funds the following month.

Typically, you will receive 90% of your funds back by the 15th of the following month.

For example, for any request made before the EO March cut off (circa March 22nd) the ~90% wire would go out by April 15th. We do reserve the right to hold up to 10% of your investment until the next calendar year to finalize the audit and prevent any unnecessary back and forth, though this is not typical and we aim to finalize the full redemption within 30 days.

As a remnant of the financial crisis and people reading about gates and hedge fund lockups, some people worry about the impact of redemptions on other investors in the Fund.

In general, we are trading highly liquid markets and so do not anticipate any situation in which one investor redeeming would materially affect other investors.

In certain extreme circumstances, such as a delay in payments from 3rd-party funds, liquidity crisis, etc., the Fund may delay payment of redemptions until the Fund has sufficient assets to pay out those redemptions. We have never had an issue with this and do not anticipate this to be an issue.

To see a full list of risks associated with the Funds, please see the Private Placement Memorandum (PPM) which is available upon request or will be supplied upon submission of our Investor Information Form to proceed with an investment.

If you are investing via a self-directed IRA custodian like Equity Trust or Inspira, all redemption requests should be directed to Mutiny instead of an IRA in order to prevent delays.

To add or redeem funds, please complete our Change Form.

In order to accept additional funds or new investments, we need to receive the wires five (5) business days before the end of the month to make sure we are able to deploy the funds to our managers in a timely manner so we ask that you submit the change form no later than eight (8) business days before the end of the month.

Forms received later than eight (8) business days before the end of the month and wires received later than five (5) days before the end of the month will be held for allocation the subsequent month (e.g. If the wire is received May 29, it will be invested July 1 rather than June 1 as it was not received 5 business days prior to June 1).

If you are redeeming funds, please note there are two parts to the process:

First, your investment will be reduced/end as of the last day of the month the request is made (assuming it is done before the 8 business day cut off date). For example, if you request a redemption on May 15th, your investment will be liquidated by the amount requested on the last trading day of May.

Second, the 3rd party administrator has to calculate the monthly performance and finalize the accounting for that month before we are able to send the full amount of your redemption.

Because we need all of our managers to finalize their accounting before we can finalize ours, this is unlikely to be completed before the 20th of the month and usually happens around the 25th-30th. Given this, our standard practice is to wire out 90% of your estimated capital account amount around the 10th-15th wires of the month. The remaining 10% of funds would go out after accounting is finalized, usually around the end of the month. In our example here of a request made on May 15th, the first wire would go out around June 10th-15th with 90% of the value. The second wire would go out around June 30th with the remaining balance.

Please be advised that this means any redemption request received inside of eight (8) business days prior to the end of the month (say May 29th) would mean your investment would remain active through the end of the following month (June 30), and the withdrawal redemption amount would be wired out the month after that (July in our example).

We anticipate you will typically receive your monthly statement around the 25th of the new month depending on how long it takes our sub-advisors to complete their monthly close process. We will also provide an estimate on the 1st of each month via our email distribution list which investors are automatically added to.

If you are not receiving the monthly estimate or the updated statement, please email invest@mutinyfund.com.

Each month, investors will receive a statement from our Third Party Administrator similar to the one below. Statements should come out around the 25th of the month. They will typically look similar to the below:

We have annotated the document with the blue text to explain each line item.

To help clarify what each of the line items represents:

Please note that all our funds use a high watermark or benchmark. In the case of a high watermark, investors are only assessed an incentive fee on net new profits. As an example, if you were to invest $100k and the value of your investment goes down to $95k then up to $105k, you would only pay the incentive fee on the $5,000 gain from $100k to $105k.

This means that depending on when someone invests, they will receive different returns than someone who invested at a different time. We try to account for the high watermark in the public number in the Tortuga Times or first of month estimates email but given everyone began investing at a different time, there will likely be discrepancies between the public numbers and your statements. Your statement number is the one you should rely on for tracking your personal investment’s value.

We can provide access to an online portal. Please note that the fund only strikes a Net Asset Value (NAV) at the end of each month, so this number will not change other than the one day per month when we will also send out your statement via email. That means the portal will not give you any additional information to what you will receive via email, merely let you access it in your browser as opposed to in an email.

If you would like access to the portal as a reference then we are happy to facilitate that. Simply complete the form at the bottom of this page and select the “I want access to the portal with my monthly statements” option from the drop-down menu.