The goal for the Volatility Strategy is to attempt to have flat or only slightly negative returns in non-volatile years for the market while achieving substantial 25-50% returns in very volatile years. The Volatility Strategy uses an ensemble of long volatility focused hedge funds which seek to create this payoff profile.

Said another way, we designed the Volatility Strategy to be convex in the event of a crisis. That means if the markets go down -10%, the volatility strategy may not post significant gains and could even have losses. However, if the markets go down 30%, we would hope for the Volatility Strategy to be up 30%+ as the convexity kicks in. Of course, it is impossible to know this a priori, but, we have constructed the portfolio with this in mind.

The convexity of the strategy is achieved through the structure of the instruments that they employ such as VIX futures and options. For example, the last week of February 2020 – the stock market fell -7%, and the VIX (for sake of easy math) spiked +70%. However, the VIX didn’t spike 10% for every 1% down move in stocks. It maybe did 5%, then 15%, then 35%, and so forth. The VIX increases non-linearly, that is, at an increasing rate. That structure creates convexity in our return profile.

Similarly, the sub-managers who buy options have a set price they pay for an option, but the amount they can gain on the option is unbounded. They can earn 1 to 1, 5 to 1, or 100 to 1, depending on the speed and extent of a given market move. Because they are buying options, there is an asymmetry: gains are uncapped while losses are capped. They can’t be wrong and lose 1 to 100, they can only lose the premium they pay for the option.

In short, the convexity of the portfolio is driven by sub-managers targeting an unbounded, asymmetric payoff structure for the amount of risk they are taking.

The question of how much you should invest is, of course, unique to your situation and nothing we say here is a substitute for speaking with a financial advisor or the use of your own judgment. Having said that, we can offer a few ways of how we personally think about it.

We believe that the best combination of offensive assets and defensive assets is approximately equal weight as embodied in our Cockroach Strategy.

In that framework, long volatility accounts for approximately 25% of the total exposure across the portfolio. Investors wishing to follow that guideline would then need to allocate ~25% to the Volatility Strategy.

For investors that wish to use the Volatility Strategy in some other way or to customize the weightings, we can offer this guidance.

We designed the Volatility Strategy to be convex in the event of a crisis. That means if the markets go down -10%, the Volatility Strategy may not post significant gains and could even have losses. However, if the markets go down 30%, we would hope for the Volatility Strategy to be up 30%+ as the convexity kicks in. Of course, it is impossible to know this a priori, but, we have constructed the portfolio with this in mind.

As a simple example, if you have a portfolio that is 90% stocks and 10% Volatility Strategy, then a 30% decline in stocks with an offsetting 30% increase in Volatility Strategy would lead to the overall portfolio being down 24% rather than 30% (compared to if it was 100% allocated to stocks). To more fully offset risks in short volatility instruments like stocks would likely require a larger allocation.

Of course, your investment amount is a personal choice and you should consult with your financial advisor and exercise your own good judgment.

Based on our research, we believe that:

To take these points in turn:

We believe a portfolio is better with a long volatility allocation.

Most investors begin with the question, what is the best possible asset to own? We start with a question that seems only slightly different but leads to a much different conclusion than what most investors own: What is the best possible portfolio to own?

As a simple example, let’s say you have the ability to buy two assets out of a possible three choices.

The first two assets (Zig and Zog) have positive returns but are highly correlated; they track one another and the business cycle. Both do well when markets are up and poorly when markets are down.

The third asset (Zag) loses money overall. It has a slightly negative return. However, while Zag loses money overall, it makes profits in periods where markets, along with Zig and Zog, are falling. That is, its most substantial gains are reserved for the periods when the other assets are in crisis.

If you can only buy one asset, Zig or Zog seem like the two best choices.

But, if you can buy two, what is the best overall portfolio?

Counterintuitively, the portfolio that combines the worst performing, but negatively correlated asset (Zag) with Zig outperforms from a risk-adjusted perspective.

In this example, by combining Zig and Zag, which are negatively correlated to each other, when Zig goes down, Zag tends to go up, and vice versa.

If you are rebalancing between the two assets, you are effectively buying low and selling high. When Zig is doing well and Zag is losing money, you are selling some of Zig to buy some of Zag.

Vice versa, when there is a market crash and Zig loses value, Zag increases and so you are selling Zag to buy more of Zig at reduced prices. That means when the market rallies, you will own more of Zig and participate in more upside.

By combining Zig & Zag, you generate better risk-adjusted, long-term returns than Zig & Zog. Though it’s counterintuitive, that is how the math works out and why we believe that diversification is so important.

If you want to increase your returns, we believe you are much better off adding a modest amount of leverage to the properly diversified portfolio (Zig and Zag) rather than using a portfolio that has correlated risks (Zig and Zog).

Assuming correlations hold, Portfolio Zig & Zag is less susceptible to blow-up risk or large declines, so you know that money will be there when you need it. If an investor has to eventually reduce their exposure because of losses, or because of retirement, or a lost job, or because a loved one got sick and needed an expensive treatment, they will probably be happier to have the Zig & Zag portfolio.

In this example, assets Zig and Zog are intended to reflect the performance of short volatility assets (stocks, bonds, real estate, VC, PE, etc.) and Zag is a long volatility asset such as the Volatility Strategy. The combination of the two outperforms either individually.

Our Volatility Strategy seeks to perform the role of Zag, performing well when the rest of your portfolio struggles. The Volatility+Stocks Strategy seeks to function similarly to the Portfolio of Zig & Zag.

Our Cockroach Strategy seeks to provide a fully diversified portfolio via a single vehicle and so may be most appropriate for investors seeking a single solution rather than wanting to use the Volatility Strategy as part of a broader DIY approach.

There are lower fee options that are designed to offer long volatility strategies which perform like Zag.

However, in our experience, passive long volatility strategies are inferior over the long run when compared to more actively managed strategies. While net of fees, passive stock and bond strategies can be very effective, we have not found this to be the case in the long volatility space where we believe active management is worth the additional costs. Please see our post on What is the VIX and how is it traded? for more information on the challenges of passive long volatility strategies.

The skill that we’re paying our sub-managers for is being able to do better than a passive approach over the course of a full market cycle (typically 5-10 years). We believe they can offer more upside in bad years for the market, with lower bleed in good times.

You could think about buying volatility as playing Roulette. There are 36 numbers on a Roulette wheel and so, rationally, anytime someone offers you better than 1 in 36 odds, you should take that bet because it is a positive expected value.

If you could place a bet that paid off 100 to 1 for number 23, that’s a good bet even though you are unlikely to win. You can think about the vol market like a Roulette wheel where the croupier, the market, has a short memory. If 17 came up three times in the last 10 spins, then you may only get 5 to 1 odds for 17 because the market is worried about another 17.

However, you may get 100 to 1 on 23 because there hasn’t been a 23 in quite some time. What our sub-managers are doing is going around and looking for the 23s, the relatively cheap vol which helps us to maintain the convexity while managing our carry costs in good years. This introduces the risk that there will be periods where 23 will not come up as much as expected and so they will underperform more passive approaches, but over the long run, we believe they will be able to take advantage of market inefficiencies and achieve superior risk-adjusted returns.

Because these strategies are capacity constrained and it requires a great deal of skill, we believe those sub-managers can demand and justify their fees.

The Volatility Strategy was initially launched within the Long Volatility Fund, LLC on April 17th, 2020. As of January 1st, 2025, the strategy is offered within the Cockroach Fund, LLC.

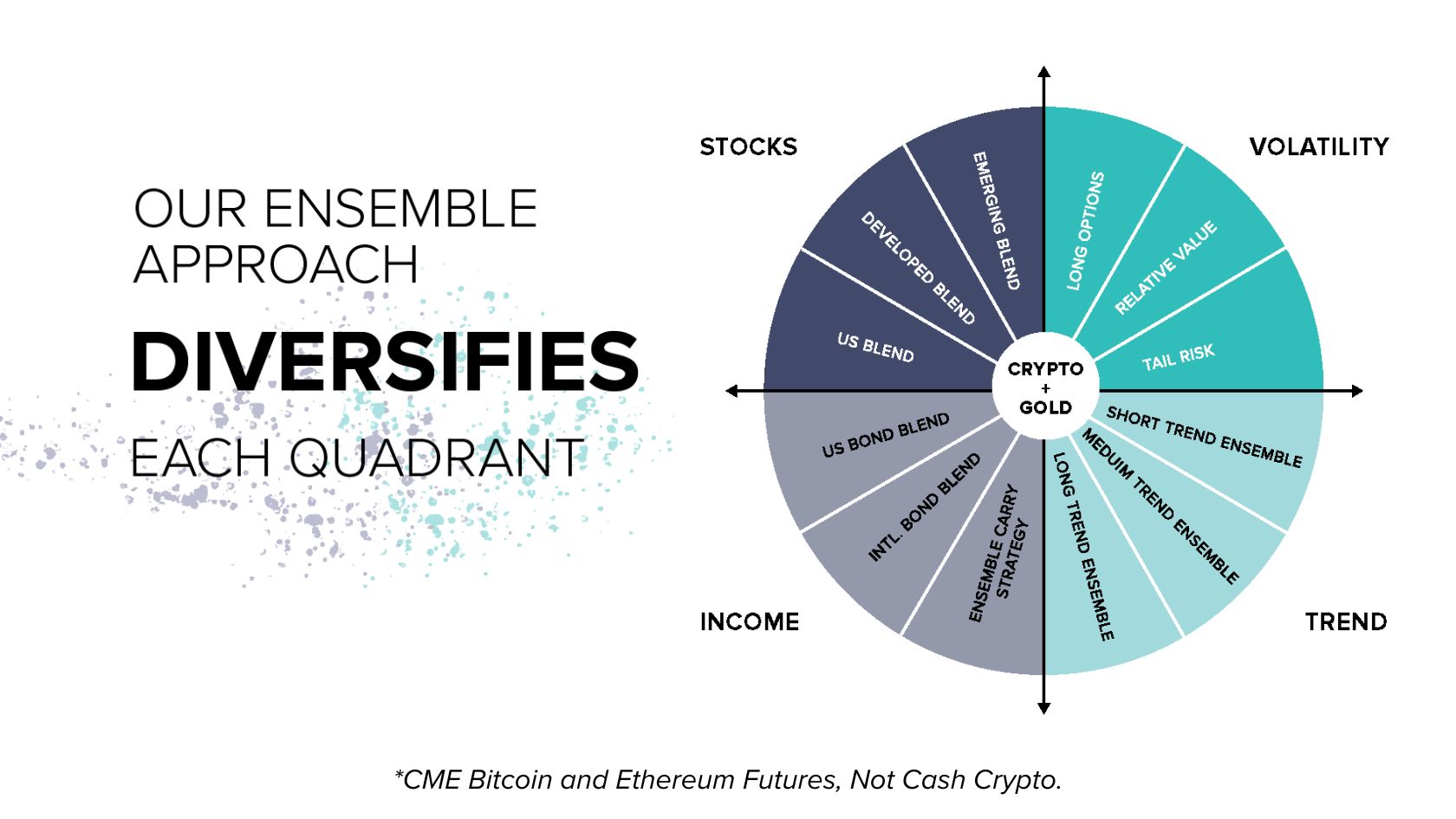

We choose sub-managers by first identifying the broader universe of long volatility managers and doing due diligence, reviewing data, decks, phone calls, and in person meetings. We then classify them into one of our three sub-strategies:

We build the portfolio around our Long Options sub-managers as the core. We like long options because we view them as a form of “debit card investing”, which acts as a sort of non-recourse leverage. That is, long options positions have the potential to return 10 to 1 or even 100 to 1, but you can only lose the principle that you pay in.

We have the largest percentage of the strategy allocated to long option strategies as they provide the most convexity and tail risk protection. They also typically have the most bleed associated with them and rely on spikes in volatility to perform.

Around the Long Options sub-strategy, we added our Relative Value sub-strategy.

The Relative Value strategy can profit in up markets, attempting to provide an income stream that helps us to achieve a positive carry over a risk-on cycle. Our implementation of relative value managers is different from other relative value strategies because we seek out managers that have a ‘long volatility bias’ to their trading strategies. That means they can flip and go long volatility so they can also do well in a crisis event along with the rest of the portfolio. We believe that combining it with our existing strategies further improves the overall return profile.

Finally, we include our Tail Risk sub-strategy. Like the Long Options sub-strategy, they offer a good deal of convexity in the case of a sharp sell-off. However, they are different in that they offer a type of ‘always on’ protection.

Our Long Options sub-managers engage in some form of market timing which seeks to limit their losses and increase their gains. This timing usually involves a reliance on market data and so may not necessarily catch exogenous events. For instance, an exogenous event like a war breaking out on a Sunday would not be reflected in any market data from the prior trading day on Friday. The Tail Risk sub-strategy accepts the slightly higher bleed that can be associated with ‘always on’ protection in exchange for being able to protect against exogenous ‘tail risk’ events such as war or, dare I say, an unexpected pandemic.

Within each of these sub-strategies, we aim to have multiple sub-managers to diversify the idiosyncratic risk of any single sub-manager. We also have different flavors of market microstructures which we believe should improve the risk-adjusted return of the Volatility Strategy. For example, one sub-manager in our relative value sub-strategy could trade exclusively U.S. markets while another trades European and Asian markets.

All of this allows us to cover more potential path dependencies with the goal of maximizing our probability of capturing any sort of risk off event with a convex return profile while not bleeding too much in good years for the market.

We feel that this structure is the best combination of the three components we want out of a long volatility strategy:

Generally, we think of each sub-strategy in this way:

We believe that our ensemble approach of multiple sub-strategies will allow us to achieve a strategy which will be roughly flat over the course of a bull market cycle (3-7 years) while exhibiting a high certainty of convex returns in the case of a major sell-off.

We have hosted many of our managers on the Mutiny Investing Podcast. You can download the podcasts on your favorite podcast app or listen/read the transcripts on our website.

Note: Manager composition is subject to change without notice.

We built the core of the portfolio around buying options. An option is a financial instrument that allows investors the right, but not the obligation (hence the option) to buy or sell an underlying asset at a specified time at a specified price.

For example, if there is a stock currently trading at $100, you could buy a put option for the right to sell the asset at a specified time (say the end of next month) at a specified strike price (say $90).

Let’s say this option costs $1. So, you pay $1 up front for the right to sell the stock for $90 at the end of the coming month. If the price of the stock falls to $85 in that time period, you can buy the stock for $85 in the open market and use your option contract to sell it for $90, pocketing a $4 profit: ($90-$85)-$1 that the option cost you.

If the stock ends the month at any price higher than $90, then the option expires worthless and you lose the $1 you paid for the option.

We like buying options because they have a fixed downside (the $1 this example) but an uncapped upside. It is a form of “debit card investing” – you can’t lose any more than you spend.

The benefit of options is that they function as a form of non-recourse leverage. You get convex exposure in the way you would if you used leverage, but unlike using leverage, your downside is capped – you don’t have to risk any more than the premium you put in.

You could think about buying options as playing Roulette. There are 36 numbers on a Roulette wheel and so, rationally, anytime someone offers you better than 1 in 36 odds, you should take that bet because it is a positive expected value.

If you could place a bet that paid off 100 to 1 for number 23, that’s a good bet even though you are unlikely to win. You can think about the vol market like a Roulette wheel where the croupier, the market, has a short memory. If 17 came up three times in the last 10 spins, then you may only get 5 to 1 odds for 17 because the market is worried about another 17.

However, you may get 100 to 1 on 23 because there hasn’t been a 23 in quite some time. What our sub-managers are doing is going around and looking for the 23s, the relatively cheap vol which helps us to maintain the convexity while managing our carry costs in good years. This introduces the risk that there will be periods where 23 will not come up as much as expected and so they will underperform more passive approaches, but over the long run, we believe they will be able to take advantage of market inefficiencies and achieve superior risk-adjusted returns.

We use an ensemble of sub-managers trading different options strategies in different markets to give us diversified exposure to options strategies, with both calls (bets on the market going up in a volatile way) and puts (bets on the market going down in a volatile way).

The Relative Value strategy can profit in up markets, attempting to provide an income stream that helps us to achieve a positive carry over a risk on cycle. Our implementation of relative value managers is different from other relative value strategies because we seek out managers that have a ‘long volatility bias’ to their trading strategies. That means, they can flip and go long volatility so they can also do well in a crisis event along with the rest of the portfolio.

One example of a relative value sub-strategy we employ is to trade the relative value between the VIX and S&P or the VIX calendar term structure. For instance, a volatility arbitrage strategy might be long the VIX and long the S&P at the same time because the VIX and S&P tend to be anti-correlated. This means that if equity prices fall sharply, they would benefit from the pickup in volatility on the VIX side but lose money on the S&P side.

The sub-managers we use here are using their proprietary algorithms to know when they want to be in the market and how to ratio the trades appropriately. If the market falls sharply and you have more exposure to the VIX than the S&P then your gains on the VIX will overcome your losses on the S&P. Getting this ratio and positioning right is what our sub-managers have spent their careers focusing on.

We also employ some short-term trend following approaches as part of this sub-strategy. One place where options struggle is after the first leg down in markets such as after the Lehman collapse in 2008. At that point, options have become more expensive because suddenly everyone wants to buy insurance. This is great for our Long Options sub-managers: we have all the long options and other people are scrambling to buy them and willing to pay up so the option sub-managers can perform really well in that first leg down.

However, after the crisis, it means that options are likely to be more expensive. If you were buying options for $1 with a max payout of $10 going into the crisis, you had 10x upside. Once options prices go up, that same option with a $10 upside may cost $3 or $4, so you have more like 2x or 3x upside. Options can still do well, but don’t have the same level of convexity at that point.

The short-term trend following approaches in our relative value sub-strategy can do well in this environment. They can go long and short on the futures indices such as the S&P in the United States or DAX and Hang Seng globally.

Shorting is structurally different from buying an option in that the return profile is the same regardless of recent volatility in the market. It doesn’t cost you anymore to go short after a 20% down move than it does during a low volatility period. That means short futures can help after we have a significant first leg down in markets to seek to increase our ability to provide returns as the market declines.

These strategies can also do well in the first leg down as well, though they will not have the same level of convexity as the options sub-strategy given the instruments they are trading.

In keeping with our belief about broad diversification and using an ensemble approach, we include managers that do other variations on these approaches with a long volatility bias.

Finally, we include a Tail Risk sub-strategy alongside our other three strategies. Unlike our Long Options sub-managers which are coming in and out of the market at different times and in different sizes, the Tail Risk sub-strategy is in the market 24/7 and 365 days a year. This offers us increased certainty in the case of a large sell off.

All of the active sub-managers in our other strategies are providing a valuable service because they are using their proprietary experience and algorithms to try and outperform passive long volatility approaches.

We believe that combining sub-managers in an ensemble approach helps to increase the odds that they are going to capture an event. Because we are using multiple sub-managers across multiple strategies, if one or two sub-managers miss a big sell off, the ensemble can still do well as others would catch it.

However, our other sub-managers are typically engaging in some form of market timing which seeks to limit their losses and increase their gains. This timing usually involves a reliance on market data and so does not manage exogenous events. For instance, a war breaking out on a Sunday would not be reflected in any market data from the prior trading day on Friday. The Tail Risk sub-strategy accepts the slightly higher bleed that can be associated with ‘always on’ protection in exchange for being able to protect against exogenous ‘tail risk’ events such as war or, dare I say, an unexpected pandemic.

This should help us protect against an exogenous event that our sub-managers’ algorithms won’t pick up as it’s not showing up in market data such as a 9/11 style event. It also enhances our convexity in the case of a sharp selloff.

There is a good deal of room for the strategy to scale, given the desire and ability to add sub-managers and further diversification across each ‘sub-strategy’. The main limiter to the scale and strategy capacity will be the capacity of sub-managers themselves, and exchange position limits across the total portfolio; however, we currently believe capacity constraints wouldn’t be experienced until around $1 billion in assets.

The question of what you should invest in is, of course, unique to your situation. Nothing we say here can or should be considered a substitute for speaking with a financial advisor and the use of your own judgment. Having said that, we will offer a few ways of how we personally think about it.

In our opinion, the Cockroach Strategy is the best liquid total portfolio solution for those looking to maximize long-term compound growth while reducing drawdowns.

The way we look at it is that the best portfolio should perform across all major macroeconomics environments: Growth, Deflation, Decline and Inflation.

We believe that this requires roughly equal parts offense and defense.

Offensive assets would be assets such as public equities, angel, private equity, and real estate.

Defensive assets would be assets such as the Volatility Strategy, gold, commodity trend strategies, and cash.

The Cockroach Strategy seeks to provide exposure to a diversified ensemble of offense and defensive assets in a liquid portfolio.

In our view, Mutiny Funds’ other offerings including the Defense Strategy, Volatility Strategy, Volatility+Stocks Strategy, and Commodity Trend Strategy are best used as tools for investors which want to customize other parts of their portfolios within the Cockroach framework.

For instance, an investor that focuses on stock selection and wants discretion over the stock portion of their portfolio could do so as they see fit and use the Volatility Strategy, Trend Strategy, or Defense Strategy to complement it and provide their defensive exposure.

Similarly, an investor focused on income from Real Estate may want to manage the Income component themselves through their real estate holding and could use the Volatility+Stocks Strategy as well as the Trend Strategy to round out the portfolio.

Of course, you may have differing views on what the appropriate portfolio construction is for your situation and should allocate using your own judgment.

In the Cockroach Strategy, we will automatically rebalance the assets each month. For investors wishing to implement themselves, we believe they must rebalance regularly to achieve the best results. This means adding to the strategies when they are losing money as well as redeeming when they are performing well.

If you are investing through a retirement account, the rebalancing can be difficult to do since sometimes new funds cannot be transferred in when you would like to and so the Volatility+Stocks Strategy or Cockroach Total Portfolio Strategy may be more appropriate as the rebalancing is done “in house.”

We don’t believe in trying to time our exposures. For instance, Calpers missed a billion dollar payday in March 2020 when they redeemed their tail risk exposure just months before. Our philosophy is that investors should focus on building a balanced portfolio rather than trying to time macroeconomic trends.

Rather than engaging in market timing, we believe it is important to remember that the Volatility Strategy, Trend Strategy or any other component of the Cockroach Portfolio should be seen as part of a broader portfolio and viewed holistically.

There will be periods where Mutiny Funds’ Volatility Strategy or any long volatility strategy underperforms short volatility strategies and/or outright loses money. Similarly, there will be periods where Mutiny Funds’ Commodity Trend Strategy underperforms or suffers losses. However, what matters is how it is performing its role in the portfolio. If a long volatility strategy is struggling while the rest of the portfolio is doing well, that’s nothing to be unhappy about – indeed that is part of its role.

We strongly believe that the combination of long and short volatility strategies will produce the best risk-adjusted returns over the long run of a lifetime, a form of True Diversification.

In the normal course of business, we are able to offer monthly liquidity. That means that if we get 8 business days’ notice before the end of the month, we are able to send the majority of your funds the following month.

Typically, you will receive 90% of your funds back by the 15th of the following month.

For example, for any request made before the EO March cut off (circa March 22nd) the ~90% wire would go out by April 15th. We do reserve the right to hold up to 10% of your investment until the next calendar year to finalize the audit and prevent any unnecessary back and forth, though this is not typical and we aim to finalize the full redemption within 30 days.

As a remnant of the financial crisis and people reading about gates and hedge fund lockups, some people worry about the impact of redemptions on other investors in the Fund.

In general, we are trading highly liquid markets and so do not anticipate any situation in which one investor redeeming would materially affect other investors.

In certain extreme circumstances, such as a delay in payments from 3rd-party funds, liquidity crisis, etc., the Fund may delay payment of redemptions until the Fund has sufficient assets to pay out those redemptions. We have never had an issue with this and do not anticipate this to be an issue.

To see a full list of risks associated with the Funds, please see the Private Placement Memorandum (PPM) which is available upon request or will be supplied upon submission of our Investor Information Form to proceed with an investment.

If you are investing via a self-directed IRA custodian like Equity Trust or Inspira, all redemption requests should be directed to Mutiny instead of an IRA in order to prevent delays.

To add or redeem funds, please complete our Change Form.

In order to accept additional funds or new investments, we need to receive the wires five (5) business days before the end of the month to make sure we are able to deploy the funds to our managers in a timely manner so we ask that you submit the change form no later than eight (8) business days before the end of the month.

Forms received later than eight (8) business days before the end of the month and wires received later than five (5) days before the end of the month will be held for allocation the subsequent month (e.g. If the wire is received May 29, it will be invested July 1 rather than June 1 as it was not received 5 business days prior to June 1).

If you are redeeming funds, please note there are two parts to the process:

First, your investment will be reduced/end as of the last day of the month the request is made (assuming it is done before the 8 business day cut off date). For example, if you request a redemption on May 15th, your investment will be liquidated by the amount requested on the last trading day of May.

Second, the 3rd party administrator has to calculate the monthly performance and finalize the accounting for that month before we are able to send the full amount of your redemption.

Because we need all of our managers to finalize their accounting before we can finalize ours, this is unlikely to be completed before the 20th of the month and usually happens around the 25th-30th. Given this, our standard practice is to wire out 90% of your estimated capital account amount around the 10th-15th wires of the month. The remaining 10% of funds would go out after accounting is finalized, usually around the end of the month. In our example here of a request made on May 15th, the first wire would go out around June 10th-15th with 90% of the value. The second wire would go out around June 30th with the remaining balance.

Please be advised that this means any redemption request received inside of eight (8) business days prior to the end of the month (say May 29th) would mean your investment would remain active through the end of the following month (June 30), and the withdrawal redemption amount would be wired out the month after that (July in our example).

We anticipate you will typically receive your monthly statement around the 25th of the new month depending on how long it takes our sub-advisors to complete their monthly close process. We will also provide an estimate on the 1st of each month via our email distribution list which investors are automatically added to.

If you are not receiving the monthly estimate or the updated statement, please email invest@mutinyfund.com.

Each month, investors will receive a statement from our Third Party Administrator similar to the one below. Statements should come out around the 25th of the month. They will typically look similar to the below:

We have annotated the document with the blue text to explain each line item.

To help clarify what each of the line items represents:

Please note that all our funds use a high watermark or benchmark. In the case of a high watermark, investors are only assessed an incentive fee on net new profits. As an example, if you were to invest $100k and the value of your investment goes down to $95k then up to $105k, you would only pay the incentive fee on the $5,000 gain from $100k to $105k.

This means that depending on when someone invests, they will receive different returns than someone who invested at a different time. We try to account for the high watermark in the public number in the Tortuga Times or first of month estimates email but given everyone began investing at a different time, there will likely be discrepancies between the public numbers and your statements. Your statement number is the one you should rely on for tracking your personal investment’s value.

We can provide access to an online portal. Please note that the fund only strikes a Net Asset Value (NAV) at the end of each month, so this number will not change other than the one day per month when we will also send out your statement via email. That means the portal will not give you any additional information to what you will receive via email, merely let you access it in your browser as opposed to in an email.

If you would like access to the portal as a reference then we are happy to facilitate that. Simply complete the form at the bottom of this page and select the “I want access to the portal with my monthly statements” option from the drop-down menu.