As a thought experiment, imagine 100 ladders lined up against a long wall. Each has a 10% probability of falling over.

If the ladders are spaced out and independent from one another, each being used in a different spot, the probability that all of them fall is astronomically low.

There is about a 1020x higher chance of randomly selecting a particular atom out of all of the atoms in the known universe than all the ladders falling down at the same time.

However, if we line all the ladders up next to each other and tie them together, the dynamic is different.

We have made them “safer” in the sense that the likelihood of any individual ladder falling will be much smaller. If one ladder starts to tilt, the weight of all the others will support it.

However, we will have also massively increased the chance that all of the ladders might fall down together.

If one ladder starts to tip, it causes another ladder to tip. That causes the next one then at some point there is a “phase shift” where enough of the ladders have started falling that they will bring down all the others.

In the first scenario, we have lots of moderate volatility. The chance of one ladder falling is pretty high, but we’re unlikely to see all of them fall.

In the second scenario with all the ladders tied together, we will see alternating periods of very low volatility and very high volatility. Either none of the ladders fall or all of them do.

This is a metaphor for a vast amount of the world we live in and we are seeing it play out in real-time right now.

The interconnectedness of travel routes increases the probability of pandemics such as the Spanish flu and COVID-19 and increases the speed at which they spread. Volatility goes from very low to very high.

The interconnectedness of our financial systems results in long periods of stability but then the possibility of massive and violent global market crashes.

The phrase used to describe this phenomenon in complex systems science, of which I am a long time student, is volatility clusters.

One danger of interdependencies is that in the short term, they may make systems appear more stable by getting rid of small fluctuations, but create the potential for massive “black swan” risk or blow-ups. By preventing the moderate volatility, you create the possibility of extreme volatility.

In just a little over two months, COVID-19 went from a thing that only a few people in a single Chinese province had to a global pandemic. It is unlike anything we have seen since the Spanish Flu of 1918.

We saw it happen in markets in the weeks following the outbreak of COVID-19.

One plausible explanation for what happened in markets is that some major hedge funds blew up some of their positions.

It seems that many of these were running what is called a “market neutral book.” Market neutral means they have to be long $100 of Stock A and short $100 of Stock B in the same industry. For example, if you expect Coke to outperform Pepsi, you could be long Coke and short Pepsi.

In theory, by being long and short the same amount, you should be flat if the broader market goes down. If the market goes down you will lose money on Coke but make money on Pepsi. All that matters is their relative value to each other.

However, in order to make money doing this, you have to use a lot of leverage. The difference in the performance of two similar assets is not that much. Maybe Coke only outperforms Pepsi by 3% this year. That’s not much. You need lots of leverage to make the trade sufficiently profitable for a hedge fund to do it.

Let’s say you have $1M to invest. Well, in order to generate higher returns, you lever up and trade on margin.

Let’s say you are leveraged 5 to 1 so you have $5M to invest into this strategy. If Coke outperforms Pepsi by 3% but you are levered up 5x, then you make 15% on your money. Now we’re talking.

So let’s say you go short Pepsi and go Long Coke. $2.5M is short Pepsi and $2.5M is long Coke. Great. Assuming no wild swings, you will outperform if Coke does better than Pepsi. Whether Food and Beverage stocks go down or up, as long as Coke does better than Pepsi, you’re set!

It seems foolproof until you get huge volatility and swings like we’ve seen in the past few weeks. A 20% move would force you to liquidate that Coke position. Remember, you are levered 5x, so a 20% down move wipes you out. A 20% loss on $5 million is $1 million, which is the actual amount you had to trade with. You get margin called by whoever gave you the margin loan to lever up (because they don’t want you to lose more of their money than the $1M you gave them). This forces you to sell your whole position.

What does all that selling do? It creates more volatility for everyone else in the market. What happens then? Someone else in a similar position somewhere else gets margin called and has to do the same thing again, thus creating more volatility.

Volatility begets volatility. Thus volatility clusters.

This decline in equity markets caused by COVID-19 has been the sharpest in history. Perhaps that is mere coincidence or chance, but the high levels of interconnectedness combined with debt have made the markets behave much more like the ladders that are tied together than those that are separate.

I don’t think it is a coincidence that the period from 2012-2019 was the lowest volatility period in US market history. The ladders were all tied together. Either none of them were going to tip or all of them were. For a long time, none of them tipped.

Then suddenly, they all did.

Hemingway understood this. When asked how he went bankrupt, he replied simply “Gradually, then suddenly.” Low volatility, then high volatility.

Volatility happens in our daily lives too. This is why examples such as “If you had bought Amazon stock in 1999 and held it for 20 years, you would have done great even though the dot com crashed happened” are dumb.

From 1999, the price of the stock collapsed by over 90%. The type of person that bought a bunch of Amazon stock in 1999 probably also bought a bunch of other crap stocks that went to zero and had a job in tech. In 2001, they had to sell everything to make rent. The volatility happened everywhere, all at once.

Volatility clusters.

If you are fragile (AKA non-ergodic), meaning there is some chance of blowing up as with tying all the ladders together, then it is guaranteed you will eventually blow up.

I think this is an absolutely crucial point that is not widely understood. You should always be prepared for a once in a lifetime event because, by definition, at some point in your lifetime it will happen.

You should have a bug out bag because even though the chances you need it in any given year are low, the chances of you needing it eventually are high and, critically, not having it is a huge risk.

Likewise, I wrote a post (unfortunately timely) about why most people’s portfolios are based on the last ten years, not the last 100 years. If you want to build and grow your wealth over a lifetime, you need a 100-year portfolio.

The key part of that for many investors is having exposure to some strategy or asset that benefits from volatility. Combining assets that benefit from volatility with assets that are harmed by volatility (such as stocks and bonds as we are seeing right now), an investor can do fine in all environments – high volatility or low volatility.

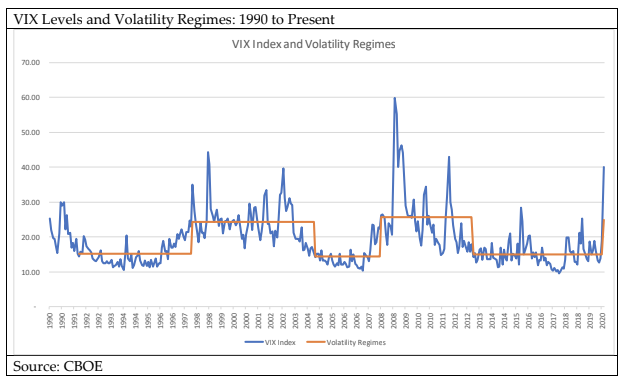

The pattern we have seen in markets is that volatility tends to cluster around a lower level, transition, and then maintain an elevated level for a period of years. This is what we would expect if markets behaved like the strung-together ladders.

Volatility was elevated from 1997-2003, then remained at low levels until 2008 when it spiked back up and remained high for 4 years through 2011.

While we saw a period of low volatility from 2012 through January of 2020 (with very occasional volatility spikes), the history of markets shows that markets tend to alternate between sustained periods of higher and lower volatility.

If history is any guide, volatility may be here to stay for quite some time.

We have not yet seen the real economic impact of COVID-19. While I am not smart enough to predict what that will be, I think it’s reasonable to believe that the story and impact will play out over a period of years rather than weeks or months and that uncertainty and volatility may remain high throughout that time.

What I do know is that volatility tends to cluster. That means there is a real possibility that it will do so this time around.

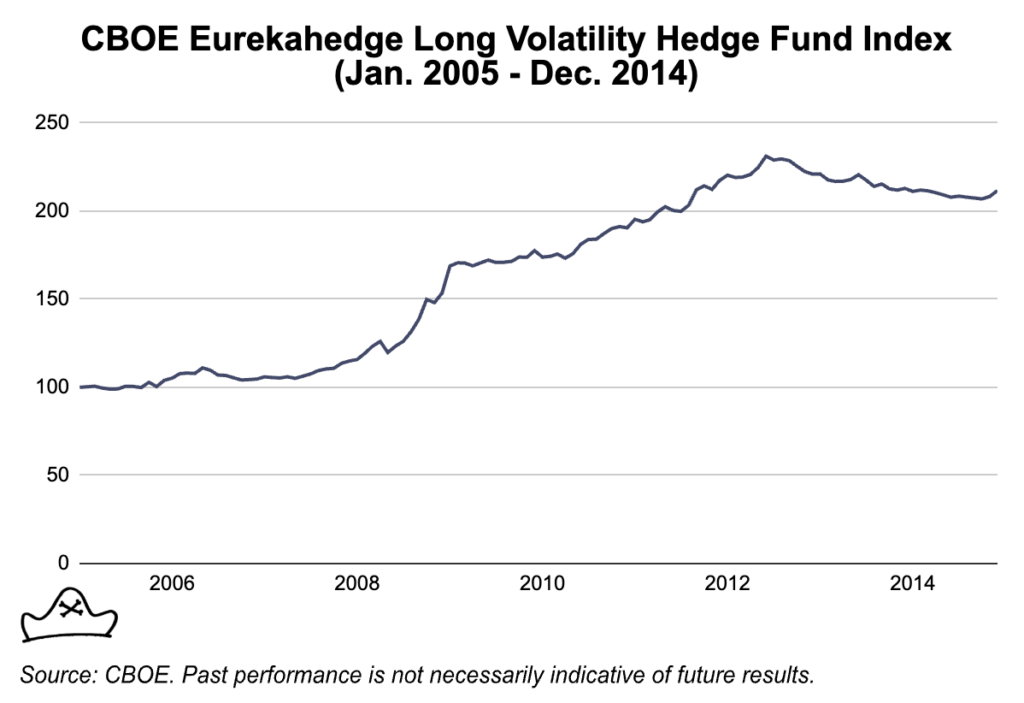

Here’s the CBOE Long Volatility hedge fund index. I think it is interesting to note that after gaining about 40% (110 to 150 on the index during the financial crisis), it went from 170 to 230 from March of ’09 to May 2012. There were 3 years of gains from volatility even after the market hit bottom.

Again, volatility clusters.

That’s great to see. It supports the point that volatility clusters and why it’s important to have portfolio exposure to assets that benefit from volatility.

Perhaps, the bigger power of long volatility exposure was that it would have let investors get back into the market at a much earlier point, knowing they had coverage should we keep going down. 2009-2011 was a great time to be buying stocks, real estate and other short volatility assets, but many were nervous that we hadn’t yet reached the bottom yet.

While I certainly can’t predict it, if volatility does cluster, it seems very possible that we will be in a similar environment for the next few years.

For most investors, there is no easy solution for buying assets that do well in highly volatile scenarios. This is the very reason we started Mutiny Funds: to find strategies that help non-institutional investors protect their portfolios from volatility. If you’re interested in learning more, please reach out via the contact form here or sign up to our newsletter.